INSIGHTS

INSIGHTS

Business Interest Deduction Limitation of Section 1063(j)

by Meaghan E. Greydanus, CPA

ARTICLE | February 03, 2025

The Tax Cuts and Jobs Act (TCJA) presents a notable change from prior law regarding a company’s ability to deduct business interest for tax years after December 31, 2017. The new Business Interest Deduction Limitation provision could potentially limit your business’s ability to deduct interest expense it paid or accrued throughout the year. Below is an overview of what the new provision entails, whom it applies to and how it is calculated.

Key Terms

Before we dive into the new provision and what it means for your business, it’s critical to understand a few key terms used in the context of this new rule.

Business Interest Expense is the amount of interest that is paid or accrued on any loans your business has taken. It does not include investment interest income or expense.

Adjusted Taxable Income is the amount of income calculated without accountable deductions allowable for depreciation, amortization, depletion, business interest, net operating losses or the new Section 199A deduction. After December 31, 2020, depreciation, amortization were depletion are no longer added back when computing adjusted taxable income.

Flooring Plan Interest Expense is the amount of interest your business has paid or accrued to acquire motor vehicles, boats or farm machinery and equipment that are held for lease or sale and are treated as inventory used to secure financing.

What is the Business Interest Deduction Limitation?

In general terms, the Business Interest Deduction Limitation states that affected businesses generally cannot deduct more than the sum of: Business Interest Expense, Floor Plan Interest Expense and 30% of the business’s Adjusted Taxable Income. For S-Corporations and Partnerships, this limit is applied at the entity level, not the owner level.

Does It Apply to Your Business?

In 2025, If your business’s average gross receipts from the past three years is less than $31 million, the rule does not apply and you will continue to have the ability to deduct business interest you have paid or accrued. If your business’s average gross receipts from the past three years are more than $31 million, the new rule does apply and a calculation will need to be done to identify how much business interest you’re able to deduct.

Businesses Excluded from the Rule

Just like with most rules, there are exceptions. If your business is engaged in certain real estate or farming activities, you may elect to be excluded from the limitation of this provision. The election, however, has consequences in the way you can depreciate your capitalized property. If your business engages in these types of activities, we can have a deeper conversation about whether this election would be a good fit for you.

How is the Limit Computed?

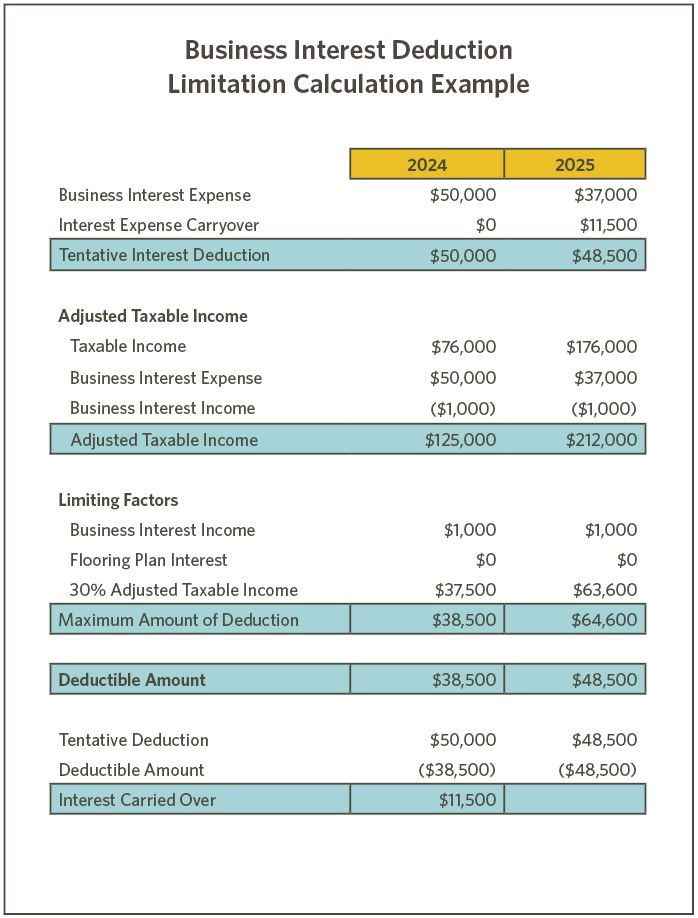

On page two, there’s an example of how the Business Interest Deduction Limitation is calculated for two tax years. As you can see, the amount of any business interest expense not allowed as a deduction for any one tax year carries over as a business expense paid or accrued in the following tax year and may be carried forward indefinitely.

Planning for the Deduction Limitation

This new rule is somewhat messy and includes complex computations to arrive at the amount a business can deduct. We can help you compute this limitation for your business, and proactively plan for how it may impact your organization.